1. INTRODUCTION

A significant size of the financial economics literature suggests that financial sector development plays a large role in economic development of any economy as it promotes economic growth by boosting capital accumulation and enhancing technological progress through increasing the rate of savings, mobilizing and pooling of savings, production of information about investments, facilitating and encouraging the inflows of foreign capital, as well as optimizing the allocation of capital. Therefore, Countries with well-developed financial systems ought to grow faster over a long period of time.

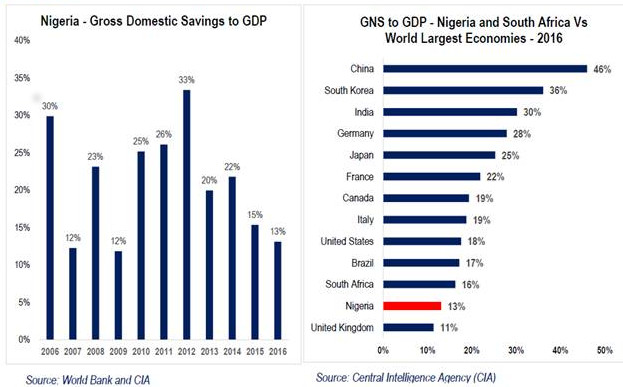

Stimulation of savings however is not as easy as it sounds. The business environment must be competitive so that business can operate profitably. In addition, savers must be assured of preservation of the real value of their savings. At the other hand, there must exist safe and profitable investments to attract savings and guarantee returns so as to preserve the real value of savers. High inflation as well as low level of saving’s rate encourage high consumption and discourages savings. Most developing economies are therefore incapable of achieving high level of savings due to high level of unemployment added to the fall in disposable income and the erosion of purchasing power which culminate into low personal savings. Nigeria’s gross national saving is low compared with most countries of the World. Based on the United States’ Central Intelligence Agency (CIA), Nigeria was placed in the 131st position out of 180 countries covered by the agency; as Nigeria’s national saving ratio was estimated to be 13.10 percent in 2016 (See figure 1 below). The national savings ratio (NSR) is the ratio of gross national savings (GNS) to the gross domestic product. This ratio portrays the saving culture. The higher this NSR, the easier it is to access low cost funds for developing long-term developmental projects. Negative NSR on its own indicate that a country is drawing from its national wealth as it is spending more than it earns.

_in_nigeria_and_nigeria_and_south_africa_in_comparison.jpeg)

Nigeria’s gross national savings as percentage of GDP has fluctuated over the years. In recent years however, it has declined through the period 1999 to 2018. It achieved a peak in 2012 at about 33 percent after which it declined with some levels of fluctuation and then declined steadily. Nigeria’s saving rate in comparison with other developed countries of the World and South Africa in 2016 is low at about 13 percent although it is slightly higher than that of United Kingdom but it is still lower than that of South Africa.

Due to this low gross savings, governments have made numerous efforts at encouraging savings. For instance, the regulatory authorities in the financial market have strengthened their regulatory and supervisory roles so as to protect savers as well as investors in the financial market. Another is the introduction of federal government of Nigeria savings bonds (by the debt management office (DMO) on behalf of the federal government of Nigeria). The creation of mutual funds and some wealth management products was pursued to stimulate savings. Other financial sector reforms have been pursued over the years in response to low saving rate, financial crisis, systemic crisis, trade liberalization, globalization, technological innovations and computerization (Akinwale 2018). The main aim of these reforms is; to ensure the creation and sustenance of sound financial practices and good corporate governance in order to ensure the attainment of sustainable economic growth and development (Onodje 2009).

Some of the reforms enacted in the Nigerian financial sector includes but not limited to: the banking ordinance of 1952, 1969 Banking Act, CBN Act No 24 of 1991 (Amended in 1997, 1998 and 1999) and the Banking and Other Financial Institutions Act (BOFIA) No 25 of 1991 (Amended in 1997, 1998 and 1999). Nigeria Deposit Insurance (NDIC) was created in 1998 through the security and exchange commission (SEC) Act of 1979, Structural Adjustment Programme (SAP) of 1988. Failed Banks (Recovery of Debts) and Financial Malpractices Decree of 1994 was established among others.

The main issue is; despite the reforms embarked upon in Nigeria over the years, the saving rate and economic growth are still low. Financial development is still not seen as making remarkable contributions to Nigeria’s economic growth thus prompting the question. To what extent is savings rate and financial development contributing to the economic growth of Nigeria? This study therefore has the objectives of finding the extent of relationship between the three measures of financial development and economic growth in Nigeria. The second objective is to find the contribution of savings to economic growth in Nigeria.

2. LITERATURE REVIEW

Onodje (2009) described financial sector as comprising of financial market institutions and insurance companies whose activities act as the heart of any economy. It consists of exchanges, financial institutions as well as brokerage houses. All these are interconnected to form the global financial market. The three segments are: money market, capital market and derivatives market (Ryan 2004, 438 – 452).

According to the World Bank (2014) financial sector consists of institutions, markets, instruments, including the legal and regulatory framework that allows transactions to be made through the extension of credit. Generally, financial sector development revolves around overcoming costs incurred in the financial system. It involves the methods of reducing the costs of acquiring information, enforcing contracts, and making transactions which culminates in the emergence of financial contracts, markets, and intermediaries. The five major functions of a financial system are: the production of information ex-ante about possible investments and the allocation of capital; the monitoring of investments and exertion of corporate governance after providing finance; the facilitation of trading, diversification, and management of risk; the mobilization and pooling of savings; and, the ease of exchange of goods and services (World Bank 2014).

The World Bank (2014) reports that financial sector development occurs when financial instruments, markets, and intermediaries ease the effects of information, enforcement, and transactions costs and then performs better job at providing the key functions of the financial sector in the economy. Levine (2005) defines financial development as information acquisition, contract enforcement, transactions’ making for the creation of incentives for particular types of financial contracts, intermediaries and market. Levine (2005) categorized the functions rendered by the financial system in any emerging market to ease transaction costs, enforcement and information under five categories. First is the provision of information ex-ante about available investments and allocation of capital. Second is the monitoring of investments and control of corporate governance after the provision of finance. Third is the facilitation of diversification, trading and risk management. Fourth is the mobilization and pools savings. Lastly is the ease of exchange of goods and services. Each of these financial functions may affect savings and investment decisions and consequently economic growth.

Rajan and Zingales (2003) defined financial development as the availability of finance to entrepreneurs for investment with adequate anticipated returns and investment risks which are shared by the financial market with low level of costs. Levine (1995) defined financial development more clearly as focusing on its function which it performs and enhances mobilization of savings in the form of; acquisition of information on investments and allocation of resources, accumulation of liquid assets, and facilitation of trade and contracts. According to Güngör, Çiftçioğlu, and Balcilar (2014) financial development means increase in the quality and quantity of financial services with lower transaction costs. On the determinants of savings, they assert that the main variable having significant effect on savings is public sector (dis)saving. This assertion is based on Ricardian Equivalence hypothesis which predicts the negative effect of public dis(saving) on private saving.

The debate on finance-growth relationship has been an age-long one from Bagehot (1873). Schumpeter (1911) proposes that productivity and growth enhancing effects of developed financial services cannot be waived aside with the back of the hand. Later Goldsmith (1969) also contributed by building the foundation of the theoretical and empirical debate on the relationship between financial development and economic growth. Solow (1956) emphasized the role of higher savings rate as a major determinant of a country’s higher per capita income. Others like Lucas (1988) and Romer (1986) also emphasized that saving rate determines the growth of an economy in the long run. They predicted that the higher the saving rate the higher will be the economic growth rate of a country. Empirical validation of the role between savings, financial development and economic growth produced plethora of studies with different focus and variable measures.

Savings play major role in supporting investment and consequently growth (Tehranchian and Behravesh 2011; Singh 2010; Alguacil, Cuadros, and Orts 2004). According to Solow (1956), the savings rate plays a crucial role in the determination of the per capita income of any country. Endogenous growth theorists like Lucas (1988) and Romer also supports the positive impact of higher savings rate on economic growth. According to Guma and Bonga-Bonga (2016) foreign capital inflows can have its merit and demerit. For instance, technological spillovers and knowledge transfer can be beneficial. However, reliance on foreign capital can be detrimental to the recipient’s economy in the form of its volatility and effect on balance of payments position which can cause instability of the recipient’s economy, hence the need for domestic savings as a necessity for economic growth (Jibrin, Danjuma, and Blessing 2014).

According to the supply leading hypothesis, rigorous activities of the financial system translates to a boost in economic growth. Choong and Chan (2011) are also of the opinion that financial deepening enhances economic growth and simultaneously; economic growth promotes financial development. Therefore, financial intermediation serves as a conduit through which savings are allocated. For instance, Hussain and Chakraborty (2012), Nasir, Ali, and Khokhar (2014) found financial development as a major input of economic growth. Akpansung and Babalola (2012) also confirmed that financial sector development can boost economic growth through increased saving, raising allocative efficiency of loanable funds and enhancing capital accumulation Others like De Gregorio and Guidotti (1995) and Al-Malkawi, Marashdeh, and Abdullah (2012) found negative impact of financial development on economic growth.

Odhiambo (2008) investigated the relationship between savings and economic growth in Kenya using data from 1991 to 2005 applying the causality tests. He found the existence of Granger causality between savings and economic growth. He concluded that savings are important drivers of development of the financial sector. Odhiambo (2009) analyzed the relationship between savings and economic growth for South Africa between 1950 and 2005 using multi-variable causality test. He found that there is a one-way causality running from savings rate to foreign capital inflows. He also confirmed that economic growth Granger causes foreign capital inflows.

Rehman, Ali, and Nasir (2015) examined the relationship between financial development, savings and economic growth in Bahrain from 1981 to 2013 using the vector Auto Regression (VAR) model. They used to capture financial development, economic growth was captured by GDP per capita and savings measured as domestic savings/GDP. Their results showed that there is a bi-directional causality between savings and economic growth. Their study did not validate the supply leading hypothesis nor the demand – following hypothesis in Bahrain.

Elias and Worku (2015) explored the causal relationship between economic growth and savings in East Africa for the period 1981 to 2014 using the vector error correction (VEC) method and Johanson cointegration. They found significantly positive relationship between domestic savings and economic growth for Uganda and Ethiopia. The Granger causality result showed unidirectional causality running from economic growth to gross domestic savings for Ethiopia and Uganda. They concluded that economic growth accelerates gross domestic savings in Ethiopia and Uganda.

Misztal (2011) analyzed the cause and effect relationship among economic growth and savings in developed countries and emerging and developing countries from 1980 to 2010. The study used cointegration as well as Granger causality. The results of the study support the existence of one-way causal relationship running from gross domestic savings to gross domestic product in the case of developed countries as well as developing and transition economies.

Najarzadeh, Reed, and Tasan (2014) analyzed the relationship between savings (total) and non-oil economic growth in Iran using annual data from 1972 to 2010 utilizing the autoregressive distributed lag model. The study established significant positive impact of savings on total economic growth and non-oil growth. Both growths also have significant positive relationship with savings. In addition, there is a long – run bi-directional causal relationship between total and non-oil growth and savings.

Horioka and Yin (2010) attempted to find the relationship between financial development and savings based on data from 12 economies in developing Asian countries using data from 1996 to 2007. They concluded that the relationship between the financial development and savings is non-linear and humped-shape.

Wang et al. (2015) used data from 1978 to 2013 to test the effects of financial development on economic growth of China using Ordinary Least Squares. They disaggregated growth into primary, secondary and tertiary industries. They found that financial development has a negative impact on growth in general and growth in tertiary industry in particular. They also concluded that financial development has no significance impact on primary and secondary industries.

Udousoro, Eko, and Ubong (2013) tested the direction of causality between savings and economic growth in Nigeria between 1980 and 2010 using a trivariate dynamic Granger causality model. They found that growth-led savings is predominant for Nigeria. In other words, there is uni-directional causality between savings and growth in Nigeria.

Odeh, Effiong, and Nwafor (2017) empirically analyzed the impact of savings and investment on economic growth in Nigeria using data from 1970 to 2015 applying the error correction method. They found gross domestic savings, fixed capital formation, labour force and savings facilities as the main determinants of economic growth in Nigeria among other findings.

Alimi (2015) explored the relationship between financial development and economic growth of seven Sub – Saharan Africa over the period 1981 to 2013. He applies both static and dynamic panel data analysis. He found financial development and economic growth as independent. In other words, financial development did not lead to economic growth for the countries under study.

Adusei (2013) analyzed the finance-growth nexus using the dynamic generalized method of moments (DGMM) Model with panel data from 1981 to 2010 of 24 African countries. He found that there is a positive relationship between finance and economic growth and that there is a bi-directional causal relationship between finance and economic growth.

Abu (2010) conducted a study on the relationship between economic growth and savings based on data from 1970 to 2007. He found cointegration existing among variables and also concluded that saving is positively related to economic growth and causality runs from economic growth to savings.

Ayinde and Yinusa (2016) investigated the relationship between financial development and inclusive growth in Nigeria using the method of quantile regression based on data from 1980 to 2013. They also found the threshold effect of the financial development on inclusive growth is 90th percentile. They also found among other things that the impact of financial development on inclusive growth depends on the measure of financial development used. Their Granger causality results show that causality runs from inclusive growth to financial development and not vice versa.

Ewetan, Ike, and Urhie (2015) analyzed the relationship between financial sector development and domestic savings in Nigeria between 1980 and 2012 (33 observations) using autoregressive distributed lag model. In their model, three measures of financial development were collapsed into one composite measure because of their high correlation and they found that financial development has a positive and significant impact on domestic savings. Taking the financial development measures one at a time, each measure is positively related to domestic savings.

So far, the issue about the impact of financial development and savings on economic growth is far from being resolved as findings and methodologies differ from one study to the other. The most common of these methodologies used the causality tests and the relationship sought goes beyond causal relationship as the extent of contributions to growth is the most important. This study therefore uses the quantile regression and Auto Regressive Distributed Lag methods to explore the relationship between financial development, savings and economic growth for Nigeria.

3. THEORETICAL FRAMEWORK AND METHODOLOGY

It is important to examine the effects of financial development on economic growth in a simple model consistent with endogenous long-run growth model (Rebelo, 1991; Montiel 1995).

Consider the model in which aggregate production is given by and the saving rate is assumed constant.

Y=AK(1)

Where is the aggregate production which is a function of capital stock

Ḱ=I(2)

represents investment and equation (2) describes the dynamics of the capital stocks.

I=Φsy(3)

Equation (3) expresses the goods market equilibrium condition, and savings and investment are equalized. In equation (3), are diverted into consumption. That equation holds the assumption that national saving rate is constant, and the value of determines it.

ˆY=AΦS−−−(4)

Equation (4) indicates the behavior of economic growth. Therefore, innovations in financial development can change the growth rate via three channels:

(i) Improvement and efficiency in capital stock captured as increases in the parameter

(ii) Improvement in the financial intermediation (increased

(iii) An increase in the saving rate

Based on the above, we formulate the above model as:

Yt=3∑i=1αiXit+St+εt(5)

Where represents measures of economic growth, are the measures of financial development. This study utilized 3 measures as can be seen from equation 5 above. represents savings. Specifically, equation 5 can be rewritten as:

RGDPPCt= ω0+ω1BMGt+ω2DCFt+ω3DCPt+ω4GSGt+μt(6)

Where:

RGDPPC is the per capita real gross domestic product (GDP), BMG is the broad money as a percentage of GDP. DCF is the domestic credit provided by financial sector as a percentage of GDP; DCP is the domestic credit to the private sector as a percentage of the GDP; GSG is the gross saving as a percentage of GDP.

In the above model, the study used BMG, DCF and DCP as measures of financial development variables (King and Levine 1993; De Gregorio and Guidotti 1995; Berthelemy and Varoudakis, 1995). We used the real per capita GDP as a measure of growth as the dependent variable as used by Deidda and Fattouh (2002).

This study applied quantile regression because of its characteristics. Quantile regression is a statistical technique with the motive of estimating and conduction of inference about conditional quantile functions. While the classical regression models is derived from minimizing the sum of squares of residuals in order to estimate models for conditional mean functions. Quantile regression models provide the methods of estimating models for conditional median functions and other full range of conditional quantile functions. Quantile regression is capable of providing a more complete statistical exploration of stochastic relationships among random variables. In addition, it is robust to outliers unlike the OLS which is not. No normal distribution or any other assumptions of OLS is required. Lastly, it is suitable for multimodal or bimodal dependent variable (Flom 2018).

Standard linear regression method summarizes the average relationship between independent variables and the dependent variable based on the conditional mean function This kind of relationship only gives partial view of the relationship. Quantile regression describes relationship at different points in the conditional distribution of

Baum (2013) considered the relationship between the regressors and the regressand using the conditional means function The median here is the 50th percentile or quartile of the distribution. The quantile is which breaks the data into proportions: below and above:

and : in the case of the median,

Given the prediction error of the model OLS minimizes while the median regression (least-absolute-deviations-LAD) minimizes Quantile regression minimizes a sum that applies asymmetric penalties for underproduction and for over-prediction. Asymptotically, quantile regression estimator is normally distributed. Median regression is more robust to outliers than OLS. While the OLS is parametric, quantile regression is non-parametric as it avoids making any assumptions about the parametric distribution of the random process (error term).

This study also utilizes the Auto Regressive Distributed Lag (ARDL) model for its dynamic properties. All data for the study were obtained from the World Bank data 2018 and the scope of the study is from 1981 to 2015 due to data limitation.

4. RESULTS

Table 1 below shows the stationarity results of the variables used in the study. Variables RGDPPC, BMG, DCF and DCP are not stationary at level. The corresponding probability is greater than 0.05. at first difference however, the four variables are stationary as their respective probabilities indicate significance at one percent level. Variable GSG however is stationary at order zero or integrated of order zero.

Since all the variables of the model are not integrated of the same order, It is desirable to test for cointegration using the ARDL Bounds cointegrated. If the F –Statistic of Bounds test is greater than the upper bound of the actual sample size, we can then conclude that there is cointegration of variables. Table 2 below shows F –Bound statistic at k degrees of freedom to be 8.228191 with 4 degrees of freedom. The value of 8.228191 is greater than the 4.39 which is the upper bound limit at one percent, we therefore conclude that all the 5 variables of the model are cointegrated at 1% significance level. This means that viewed individually, 4 out of 5 variables are not stationary at levels, but combining them in a model, we are bound to have a stationary process.

Table 3 shows the correlation matrix of the variables of the model. This correlation is necessary as some measures of financial development are highly correlated. From the correlation result below, DCP has a correlation of about 0.79 with BMG. DCF also has a correlation of about 0.73 with BMG and the correlation between DCP and DCF is about 0.32. Two of the correlation coefficients are high though, but not so high as to cause multicollinearity in the estimates. Therefore, they can be combined as explanatory variables in the same model.

The study results of the model are presented in Table 4 in five columns. The first is; simple Ordinary Least Squares (OLS), the second is the OLS estimates with Autoregressive process. The third is the Quantile regression with median estimates. The fourth is the Quantile regression with tau of 0.75 known as inter-quartile range estimates. The fifth is the Autoregressive estimates of order (2,0,2,2,2) simulated based on 2,500 evaluations.

Column one result shows that all the measures of financial development as well as the measure of savings are significant in explaining economic growth. Broad money as a ratio of GDP significantly depresses growth while other measures of financial development as well as saving significantly boost economic growth. However, the low coefficient of determination as well as the presence of serial correlation made the study to estimate autoregressive OLS. This provided remedies to the model even though only the autoregressive term significantly aided growth. This is a testimony that OLS may not be appropriate in estimating this model.

The results of Auto Regressive Distributed Lag (ARDL) model indicate that a year lag of growth significantly aided current growth level at one percentage significance level. The first measure of financial development (Broad money as a ratio of GDP) has an inverse relationship with economic growth. This relationship is significant for semi – interquartile range and the Auto Regressive Distributed Lag (ARDL).

Domestic credit provided by the financial sector as a proportion of the gross domestic product (DCF) is significantly positive only in the semi-interquartile range. It is not significant in the quartile range and the Auto Regressive Distributed Lag (ARDL). The four-year lag of DCF is also not significant. Domestic credit to private sector as a ratio of gross domestic product (DCP) Showed a positively significant coefficient at five percentage level for Kernel quantile regression at tau equal 0.5 and 0.75. Auto Regressive Distributed Lag (ARDL) coefficients are positively related to growth at ten percentage significance level for the second and the fourth lag of DCP.

Savings in proportion to GDP (GSG) is significantly explained and positively related to growth at the semi-interquartile range. GSG contributed positively significantly to the explanation of economic growth for Nigeria in the second lag of the ARDL model. Generally, we can conclude that financial development moderately contributed significantly to the explanation of economic growth in Nigeria when financial development is captured by DCF and DCP but negative when measured by BMG. Savings also contributed fairly to the explanation of growth in Nigeria. The findings in this study are partly in agreement with the findings of Abu (2010) and Alimi (2015).

5. CONCLUSION AND RECOMMENDATION

This study set out to examine the relationship between the measures of financial development, savings and economic growth in Nigeria. It was found that two measures of financial development exert fairly significant positive relationship on economic growth in Nigeria for the study period. One measure of financial development (broad money as a ratio of GDP) exerted negatively significant impact on economic growth in Nigeria which is a mixed result. Savings exerted fairly positive impact on economic growth. This impact is significant in the current time and the second lag of savings. That means current savings have significant positive impact on future economic growth. The quadratic results portray a non-uniformity in the impact of savings because at the median growth level, savings’ impact is insignificant but at higher level of growth savings significantly contributes to economic growth suggesting that there is a threshold effect of savings on economic growth in Nigeria.

This study therefore recommends that policy makers must ensure and develop sound Macroeconomic and sectoral framework that further improves competition in banking and non- bank financial institutions so as to enhance Innovation that ultimately leads to creation of more customer- friendly financial products that will further boost economic growth.

Government at all levels must support savings mobilization drive in order to boost savings in Nigeria. Moreover, since savings comprises of private and public savings, Public savings in Nigeria is a function of oil revenue and excessive re-current public expenditure which crowds out public savings. For savings to be boosted therefore, government must adopt fiscal discipline in the public sector on one hand and must diversify the economy base to cushion the effects of volatility of its exports.